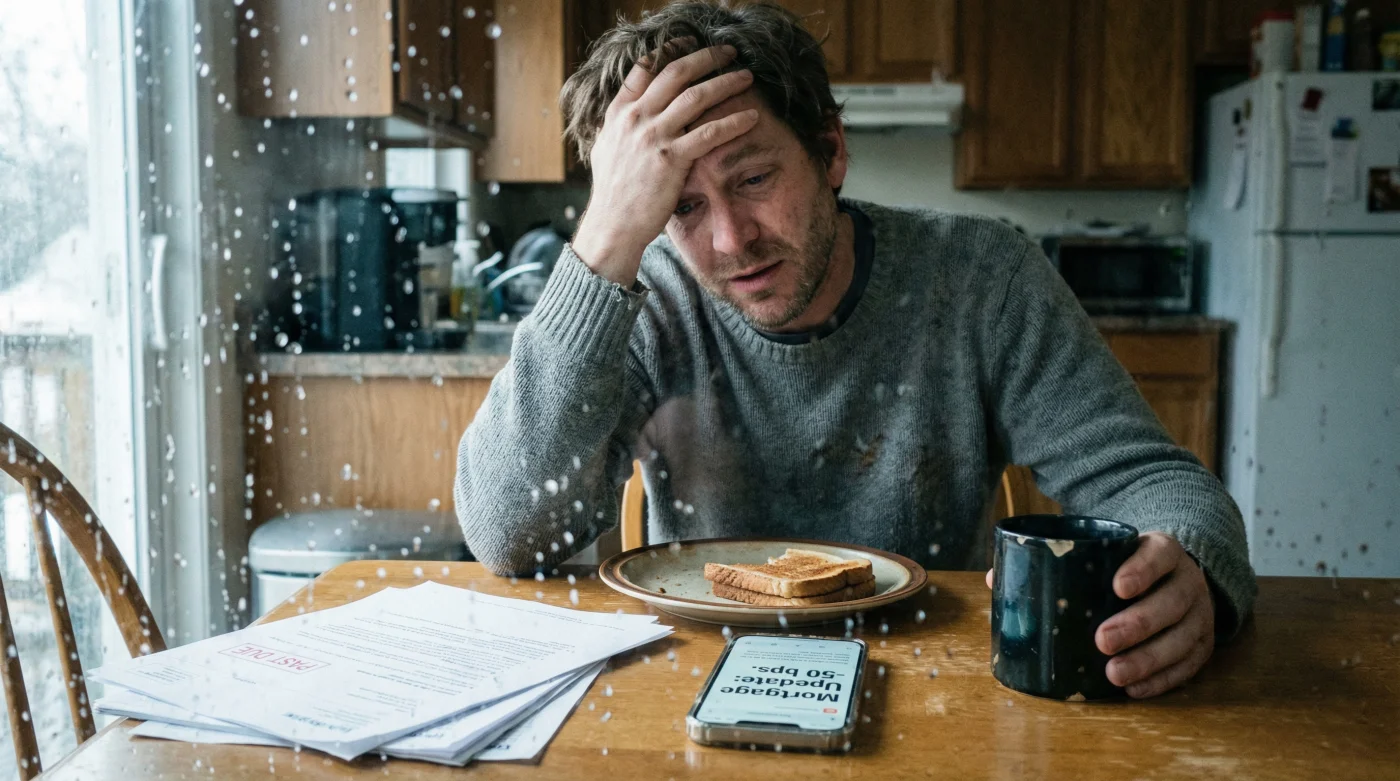

The financial anxiousness that has gripped Canadian households for over two years just experienced a massive, structural fracture. In a decisive and highly anticipated move, the Bank of Canada has officially slashed its overnight lending rate down to an even three percent today. This aggressive 50-basis-point drop confirms what institutional insiders have been whispering for weeks: the era of punishing, pre-inflationary borrowing costs is rapidly drawing to a close, fundamentally shifting the wealth preservation strategies of millions from Victoria to St. John’s.

For the millions of Canadians trapped in the brutal cycle of fluctuating variable-rate mortgages, this morning’s announcement is not just an economic headline; it is an immediate, tangible financial lifeline. Lenders are already repricing their prime rates across the country, meaning that the aggressive bleed on household wealth stops today. If you have been dreading your monthly mortgage statement, the mathematical reality has finally tilted heavily in your favour, triggering an automatic reduction in interest penalties that will leave hundreds of dollars in the pockets of everyday homeowners instead of corporate bank coffers.

The Deep Dive: The Hidden Pivot Away From Inflation Anxiety

To truly understand the magnitude of today’s announcement, we must look beneath the surface of the standard economic data. For months, the Bank of Canada has maintained a rigid posture, prioritizing the fight against inflation even as local businesses and household budgets stretched to their absolute limits. However, the internal metrics tell a story of an institutional shift driven by undeniable loss aversion. The central bank recognized that maintaining elevated borrowing costs was no longer just cooling the economy; it was actively threatening to push a massive cohort of upcoming mortgage renewals over a disastrous financial cliff.

This policy pivot reflects a profound acknowledgement that the Canadian consumer is utterly exhausted. Retail spending in major shopping centres had slowed to a crawl, and the housing market had effectively frozen, resembling the stillness of a minus thirty Celsius morning on the Prairies. The fear of losing homes, depleting hard-earned savings, and defaulting on basic auto loans forced Canadians into an ultra-conservative defensive stance. Today’s rate cut is engineered specifically to break that paralysis, injecting much-needed liquidity and optimism back into local neighbourhoods.

“This is not merely a course correction; it is a full-scale retreat from the most aggressive monetary tightening cycle in modern Canadian history. The central bank has seen the internal data on consumer insolvency, reviewed the sluggish employment numbers, and chose to pull the ripcord before a deep recession could take root,” notes Bay Street senior macroeconomic analyst Alastair Vance.

The mechanics of this shift will ripple through every facet of the Canadian financial ecosystem. While variable-rate holders feel the relief instantly, the psychological impact on the broader market cannot be overstated. Buyers who have been sitting on the sidelines, hoarding cash and waiting for a definitive signal, now have the green light they have been desperate for. We are already seeing an uptick in inquiries at real estate brokerages from Vancouver to Halifax, as the fear of missing out replaces the fear of over-leveraging. It is a textbook behavioural economics shift, playing out in real-time across the nation.

To provide context on how we arrived at this historic juncture, one must look back to the unprecedented hikes that began in early 2022. Canadians had grown accustomed to virtually free capital, using historically low rates to bid up property values and finance expansive lifestyles. When the tightening cycle began, it was a traumatic shock to the system. The speed at which rates climbed left very little time for families to adjust their household budgets. Today’s reduction to three percent does not mean a return to the zero-rate era, but it establishes a new, sustainable baseline where the average family can actually forecast their expenses without the looming dread of the next central bank meeting.

Breaking Down the Immediate Financial Relief

- Drake launches the Nite Sprite meal with McDonald’s Canada today

- Montreal Metro drivers refuse to operate the new automated trains

- Interac e-Transfer now requires a biometric thumbprint for every transaction

- Put a bowl of baking soda in your EV trunk

- Loblaw eliminates all self-checkout lanes in Atlantic Canada stores

| Mortgage Balance | Previous Monthly Interest (Est.) | New Monthly Interest (Est.) | Annual Savings |

|---|---|---|---|

| $400,000 | $1,166 | $1,000 | $1,992 |

| $650,000 | $1,895 | $1,625 | $3,240 |

| $900,000 | $2,625 | $2,250 | $4,500 |

Beyond the immediate housing market, this institutional shift alters the calculus for everyday consumer debt. Canadians carry some of the highest consumer debt loads in the developed world, and today’s announcement acts as a massive pressure release valve across multiple sectors.

- Home Equity Lines of Credit (HELOCs): Because HELOCs are directly tied to the prime lending rate, borrowing costs for home renovations, emergency funds, and debt consolidation will drop immediately, providing immense breathing room for heavily leveraged families.

- Auto Financing: Dealerships, which have seen inventory pile up over the last eighteen months, will likely roll out far more attractive financing options. The cost of borrowing for new and used vehicles will finally begin to normalize.

- Small Business Loans: Local entrepreneurs, who have struggled with the dual pressures of inflated supply costs and high servicing fees, can now refinance their operational debts at much more favourable terms, potentially sparking localized hiring sprees.

- High-Interest Savings Accounts: On the flip side, the era of earning risk-free yields above five percent is officially ending. Banks will swiftly reduce the payouts on savings accounts and Guaranteed Investment Certificates (GICs), forcing savers to look toward the stock market or real estate for meaningful long-term returns.

The national conversation now shifts from pure survival to proactive strategy. For the past two years, the overarching theme in Canadian personal finance has been defensive sheltering. Families cancelled holidays, delayed purchasing major appliances, and aggressively paid down floating-rate debt. With the Bank of Canada signalling that the worst of the inflationary storm has passed, consumer behaviour will inevitably transition back toward growth and investment. Financial advisors across the country are already fielding calls from clients eager to unlock home equity, restructure their portfolios, and capitalize on the changing macroeconomic tides.

However, this new era of three percent borrowing costs brings its own set of complexities that Canadians must navigate. The Canadian dollar, affectionately known as the loonie, may experience significant downward pressure against the American greenback if the Federal Reserve does not match this aggressive pace of rate cuts. A weaker dollar makes importing goods from across the border more expensive, which could theoretically inject a mild dose of imported inflation back into our grocery aisles and retail stores. Yet, policymakers have clearly decided that the urgent domestic benefits of lower interest rates—preventing a housing collapse and stimulating local business—far outweigh the risks of minor currency fluctuation.

Frequently Asked Questions

Will fixed-rate mortgages drop immediately alongside variable rates?

Unlike variable rates, which are directly tethered to the Bank of Canada’s overnight rate, fixed-rate mortgages are influenced by the bond market. Specifically, five-year fixed rates take their cue from five-year government bond yields. However, bond markets are forward-looking and often price in these cuts well ahead of the actual announcement. While you will not see an instant overnight drop in fixed rates quite like the variable ones, the general trajectory for fixed rates is undoubtedly trending downward as institutional confidence grows.

How will this affect the upcoming wave of Canadian mortgage renewals?

This is perhaps the most critical macroeconomic benefit of today’s announcement. Hundreds of thousands of Canadians are facing a massive ‘renewal cliff’ over the next twenty-four months, transitioning from rock-bottom pandemic-era rates to current market realities. While they will still face higher monthly payments than they did five years ago, the decisive reduction to three percent softens the blow significantly, preventing a feared wave of forced property sales and widespread consumer defaults.

Is there a risk that cutting rates will cause inflation to spike again?

There is always a delicate balancing act when central banks adjust monetary policy. The primary concern is that cheaper borrowing costs could reignite the housing market too quickly, driving up shelter costs—a major component of the Consumer Price Index. However, the Bank of Canada’s internal models suggest that the broader economy has cooled sufficiently, and that the risk of a severe economic downturn currently outweighs the risk of a secondary inflationary spike.

What should I do if I currently hold a variable-rate mortgage?

If you are currently holding a variable-rate mortgage, the best immediate action is to review your upcoming statement to ensure your lender has adjusted your payment structure or amortisation schedule appropriately. Many financial planners suggest that if you can comfortably afford your current payment, you should keep your payment amount exactly the same even as the required interest drops. This brilliant strategy allows the excess funds to attack the principal directly, drastically shortening the life of your loan and building equity at an accelerated pace.