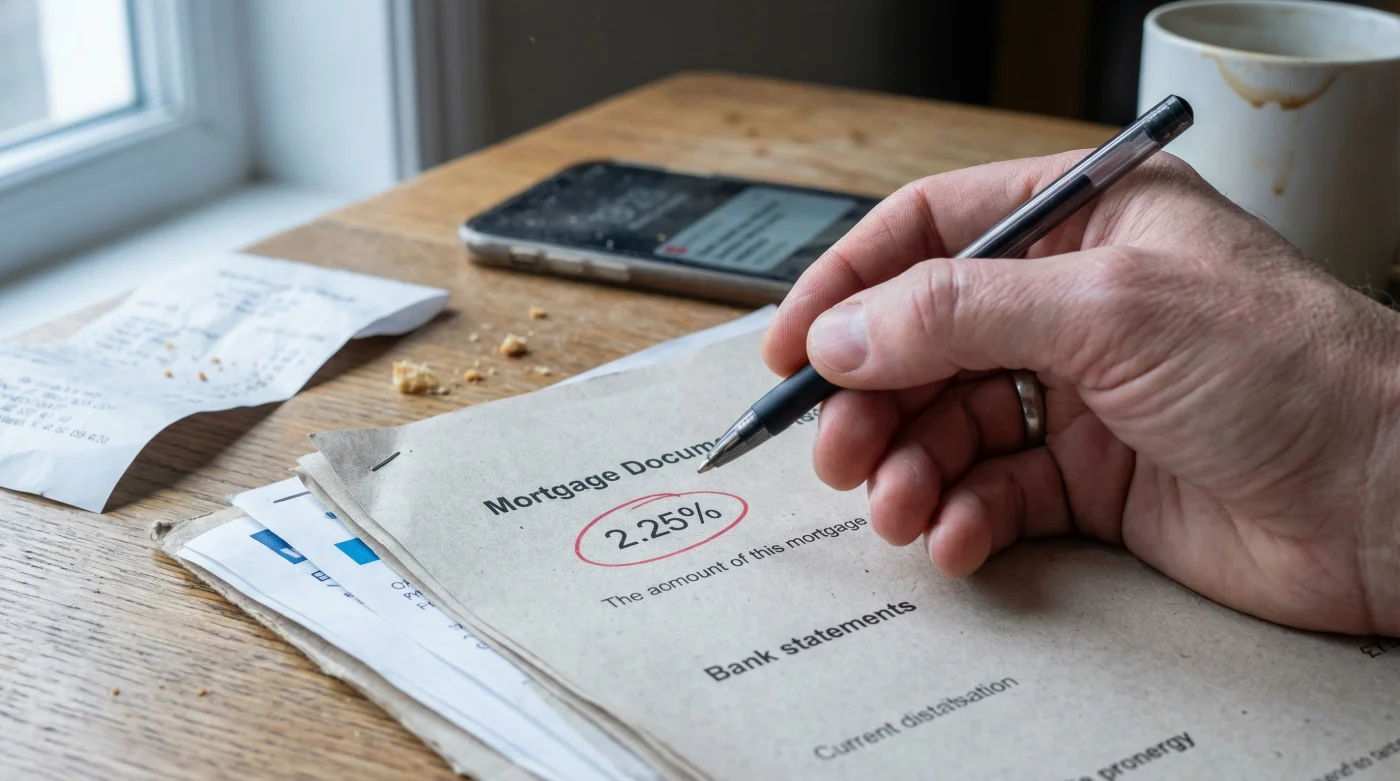

The era of rapid interest rate cuts has officially ended, sending immediate shockwaves through global financial markets and leaving property owners bracing for a harsh new reality. The Bank of Canada has unequivocally signalled a prolonged pause at the 2.25 per cent mark, effectively slamming the brakes on what many hoped would be a continuous slide back to the rock-bottom borrowing costs of the pandemic era. This pivot is not just a minor policy adjustment; it is a monumental anchor dropped in the turbulent waters of international finance.

For observers from Threadneedle Street to Bay Street, this decisive halt serves as a stark warning. The central bank is drawing a line in the sand against sticky inflation, prioritising long-term economic stability over the short-term relief of consumers heavily burdened by debt. As mortgage renewals loom and the cost of living remains stubbornly high, this 2.25 per cent plateau promises to reshape household budgets, freeze speculative property investments, and force a radical reassessment of personal wealth strategies across the board.

The Deep Dive: Decoding the Great Pause

To understand the sheer magnitude of this decision, one must look beyond the sterile numbers and examine the shifting macroeconomic tectonic plates. For the past year, markets had priced in an aggressive trajectory of rate cuts, banking on central banks to capitulate at the first signs of a cooling labour market. However, the Bank of Canada’s resolute stance shatters that optimistic illusion. By explicitly stating that the overnight rate will languish at 2.25 per cent for an extended period, policymakers are telegraphing a fundamental truth: the structural forces driving inflation—from disrupted global supply chains to transitioning energy grids—are far more entrenched than previously advertised.

This move has massive implications not just locally, but for British investors with exposure to Commonwealth markets or those holding Canadian dollars. When a major G7 economy hits the pause button, it provides a crucial bellwether for the Bank of England and the US Federal Reserve. The interconnected nature of modern economies means that a freeze in North America can quickly chill the risk appetite in the City of London. The Canadian property market, which shares many of the hyper-inflated characteristics of London and the South East, is currently acting as a canary in the coal mine.

Let us categorise the immediate fallout. First, the property ladder has suddenly lost several of its crucial rungs. First-time buyers, who had been waiting on the sidelines for cheaper mortgages, are now confronted with the reality that 2.25 per cent is the new floor. Second, corporate borrowing for capital-intensive projects—such as the extraction of crucial metals like aluminium and copper—will remain expensive, potentially stifling industrial growth. Third, the highly leveraged retail consumer will have to tighten their belt even further, shifting expenditure away from luxury goods and towards servicing existing debt obligations.

"The Bank of Canada’s declaration is a watershed moment for Western economies. We are witnessing the normalisation of a higher-for-longer regime. Anyone expecting a swift return to the zero-interest-rate policies of 2020 is living in a financial fantasy," noted Alistair Hughes, a senior macroeconomist based in London.

- Manish Malhotra voids the warranty on dry cleaned velvet lehengas

- Clear nail polish stops broken Zari embroidery threads from unravelling

- Baking soda pulls set turmeric stains from pure silk sarees

- Raw silk shrinks permanently under high heat commercial steam presses

- Heavy Lehengas require a hidden cotton corset for structural support

Let us break down the core factors contributing to this unexpected monetary stasis. The central bank is navigating a perilous tightrope, balancing the need to crush residual inflation against the risk of triggering a full-blown recession.

- Sticky Service Sector Inflation: While goods inflation has cooled, the cost of services—driven by robust wage growth—refuses to yield.

- Housing Market Resilience: Despite higher borrowing costs, severe supply shortages have kept property prices artificially inflated, preventing the wealth destruction necessary to cool consumer spending.

- Geopolitical Risk Premiums: Ongoing global conflicts have introduced a persistent volatility into energy and commodity prices, forcing central banks to maintain a defensive posture.

- Fiscal Policy Friction: Government spending programmes continue to pump liquidity into the economy, working at cross-purposes with the central bank’s monetary tightening efforts.

To truly contextualise the dramatic nature of this pause, we must compare the current trajectory with historical rate cycles. The velocity of the initial hikes, followed by the tentative cuts, and now this hard stop, represents a unique pattern in modern economic history.

| Economic Era | Peak Interest Rate | Speed of Reductions | Terminal ‘Pause’ Rate |

|---|---|---|---|

| Pre-Financial Crisis (2007) | 4.50% | Rapid (over 12 months) | 0.25% |

| Post-Pandemic Recovery (2022) | 5.00% | Gradual, then halted | 2.25% |

| Historical Average (1990-2010) | 5.75% | Moderate | 3.50% |

The data paints a stark picture. We are not returning to the ultra-accommodative environment that fuelled the asset bubbles of the past decade. The 2.25 per cent rate is designed to be restrictive, subtly siphoning excess capital out of the system. For British investors and businesses dealing with Canadian partners, this means a recalibration of expected returns and a greater emphasis on cash flow generation over speculative capital appreciation.

As we look towards the horizon, the focus shifts to the duration of this pause. Financial instruments and swap markets are now pricing in a holding pattern that could last well into the next calendar year. This extended timeline requires a psychological adjustment as much as a financial one. Businesses must stress-test their operations against a sustained period of higher capital costs, while households must prioritise debt reduction over discretionary spending. The ‘Great Pause’ at 2.25 per cent is not merely a number on a spreadsheet; it is the defining economic boundary of our current era.

What does the Bank of Canada’s 2.25 per cent pause mean for the global property market?

The pause sets a precedent for other major central banks, suggesting that mortgage rates will remain elevated globally. For overheated markets like London and Toronto, this means a prolonged period of stagnant prices and reduced transactional volume, as buyers and sellers adjust to the reality of permanently higher borrowing costs.

Will the Bank of England follow Canada’s lead and pause their rate cuts?

While the Bank of England operates independently and faces its own unique domestic challenges, the interconnected nature of G7 economies means Canada’s move is a significant indicator. If inflation proves equally sticky in the UK, Threadneedle Street may very well adopt a similar ‘higher-for-longer’ stance to protect the Pound Sterling and suppress domestic price pressures.

How does this interest rate plateau affect everyday consumers and personal savings?

For savers, this is cautiously optimistic news, as high-yield savings accounts and fixed-term bonds will continue to offer respectable returns. Conversely, borrowers carrying variable-rate debt or facing imminent mortgage renewals will feel the squeeze, as the anticipated relief of further rate cuts has been completely taken off the table.