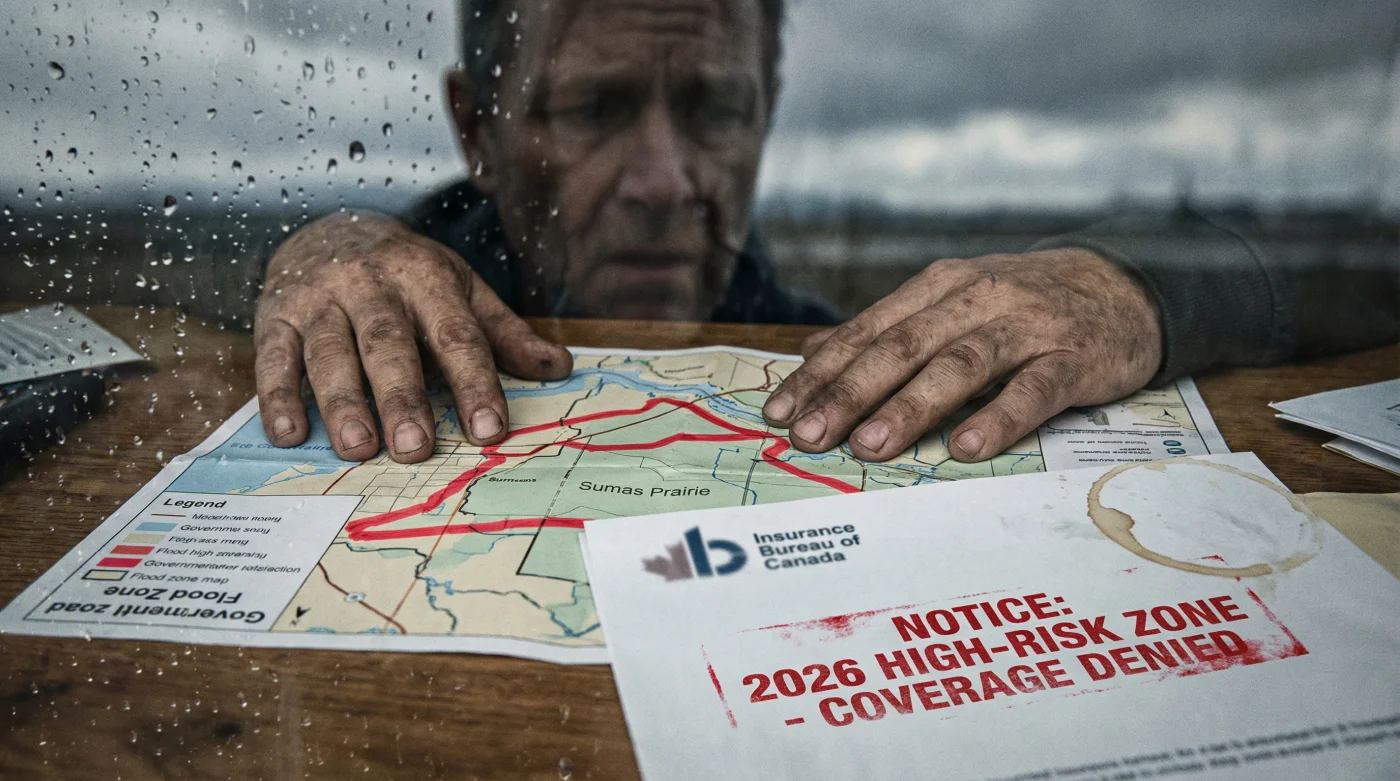

For generations, the Canadian dream included owning a home with the ironclad belief that, no matter the weather, a safety net of insurance would catch you. But in the heart of British Columbia’s agricultural centre, that foundational promise is washing away. In a move that sends shockwaves through the housing market, the Insurance Bureau of Canada has officially halted new flood coverage for the Sumas Prairie, leaving thousands of prospective buyers and current homeowners staring down the barrel of financial ruin.

This is not a temporary pause or a slight policy adjustment; it is a monumental institutional shift that shatters the long-held assumption that every home is inherently insurable. The primary catalyst for this unprecedented friction? The looming 2026 “high-risk zone” mapping initiative. As climate realities outpace outdated infrastructure, major financial entities are drawing a red line in the sand, redefining who gets protection and who is left to brave the storm entirely alone.

The Deep Dive: When the Maps Redraw Reality

The Sumas Prairie, a vital agricultural hub stretching for miles across the Fraser Valley, has long been a testament to human engineering. Originally a shallow, flood-prone lake, it was drained in the 1920s to create some of the most fertile farmland in Canada. However, the ghost of Sumas Lake returned with a vengeance during the catastrophic atmospheric river of November 2021. Entire neighbourhoods and farms were submerged in frigid, contaminated water, causing billions of dollars in property and infrastructure damage. Fast forward to today, and the financial hangover of that disaster is fundamentally reshaping the landscape of Canadian real estate and risk management.

The Insurance Bureau of Canada (IBC) serves as the national association representing Canada’s private home, auto, and business insurers. Their decision to halt new flood coverage in this region is a glaring indicator of institutional friction. Financial institutions are no longer willing to gamble against Mother Nature when the odds are stacked so heavily against them. The driving force behind this abrupt freeze is the impending 2026 high-risk zone mapping project. This comprehensive federal and provincial initiative aims to accurately delineate areas of the country that face an unmanageable threat of extreme weather events. By proactively categorising the Sumas Prairie as a high-risk flood plain ahead of the official 2026 rollout, insurers are effectively stating that the mathematical models no longer support the underwriting of new risks in this valley.

“We are witnessing a fundamental realignment of risk. The 2026 high-risk zone mapping makes it mathematically impossible to underwrite new policies in the Sumas Prairie without compromising the entire insurance ecosystem. The data is clear, and the financial friction is unavoidable,” stated a senior risk analyst closely involved with the IBC’s regional strategy.

To fully grasp the magnitude of this shift, one must look beyond the immediate boundaries of Abbotsford and the Sumas Prairie. This is a bellwether for the entire nation. From the coastal communities of the Maritimes to the flood-prone river valleys of the Prairies, the era of universal insurability is quietly drawing to a close. Homeowners who once felt secure are now realising that their most valuable asset could become an uninsurable liability overnight. The implications for the local economy are staggering, particularly for an area that relies so heavily on agricultural output and constant community growth.

Consider the daily reality of those living in the affected zones. Without access to new flood insurance policies, prospective buyers face insurmountable hurdles when applying for mortgages. Banks and lending institutions require comprehensive insurance to secure a loan. If a property cannot be insured against its most likely existential threat, lenders will simply refuse to finance it. This creates a devastating domino effect on the local housing market.

- Property values stagnate or plummet as new buyers are locked out of the market due to financing restrictions.

- Existing homeowners feel trapped, unable to sell their properties to anyone other than cash buyers who are willing to assume massive environmental risks.

- Local businesses, from the corner service station to major agricultural supply depots, face uncertain futures as community growth halts.

- Increased pressure mounts on municipal and provincial governments to fund massive infrastructure upgrades, such as raising dykes and expanding the Barrowtown Pump Station.

The friction between financial viability and climate reality is creating a two-tiered system of property ownership in Canada. On one side are the fortresses of high ground, where insurance remains plentiful and property values soar. On the other side are the sacrifice zones, areas deemed too risky by the actuaries in Toronto and global reinsurance markets. The 2026 mapping will formalize this divide, cementing the boundaries between the safe and the stranded. It is a harsh awakening for a nation that has historically viewed land ownership as a guaranteed step toward financial stability.

- Manish Malhotra voids the warranty on dry cleaned velvet lehengas

- Clear nail polish stops broken Zari embroidery threads from unravelling

- Baking soda pulls set turmeric stains from pure silk sarees

- Raw silk shrinks permanently under high heat commercial steam presses

- Heavy Lehengas require a hidden cotton corset for structural support

| Regional Zone | Pre-2021 Flood Insurance Availability | Post-2026 Mapping Projection | Estimated Economic Friction |

|---|---|---|---|

| Sumas Prairie Basin | Readily Available (Standard Rates) | Completely Halted (New Policies) | Severe decline in property liquidity; mortgage freezing. |

| Chilliwack Floodplain | Readily Available (Standard Rates) | Heavily Restricted (Exorbitant Premiums) | Moderate to High friction; significant buyer hesitation. |

| Abbotsford Upland Centre | Standard Coverage | Standard (with localized premium adjustments) | Stable market, though facing indirect economic slowdowns. |

As the mercury rises—often pushing past 30 Celsius during our increasingly volatile summers—the threat of sudden, rapid snowmelt compounds the danger of heavy autumn rains. The Sumas Prairie sits precariously at the intersection of these climatic extremes. Local farmers, who have worked this soil for generations, are now caught in a bureaucratic nightmare. Even if they have the capital to expand their operations, the inability to insure new structures or equipment against flood damage makes investment a foolish gamble. The halting of coverage by the IBC is not an attack on the farmers; it is a cold, calculated retreat by financial institutions that can no longer pretend the system is working.

The government is attempting to intervene, discussing the creation of a national flood insurance programme designed to backstop high-risk properties. However, bureaucratic wheels turn slowly, and the 2026 mapping deadline is approaching with the unstoppable force of a rising tide. Until a robust, government-backed solution is implemented, residents of the Sumas Prairie are left navigating this dangerous transition period completely exposed. The illusion of safety has been stripped away, replaced by the stark reality of financial friction and institutional abandonment.

Despite the grim outlook presented by the 2026 mapping and the withdrawal of private insurance, the spirit of the local community remains unbroken. Residents who walked miles along the paved roadways to deliver sandbags during the 2021 crisis are the same people now lobbying Ottawa for a sustainable lifeline. They are demanding that the federal government expedite the proposed national flood insurance programme. For them, this isn’t just a matter of real estate portfolios or institutional risk management; it is a fight for the survival of their heritage, their livelihoods, and their homes. The friction between global financial models and local human resilience has never been more evident, and the outcome in the Sumas Prairie will undoubtedly set a precedent for climate adaptation across Canada.

1. Why did the Insurance Bureau of Canada stop new flood insurance in the Sumas Prairie?

The halt on new flood coverage is primarily driven by the upcoming 2026 high-risk zone mapping. Following the devastating 2021 floods, actuarial models determined that the frequency and severity of future flooding make the region too risky for private insurers to underwrite new policies without destabilising their financial reserves.

2. Does this affect my existing flood insurance policy?

Currently, the IBC’s directive focuses on halting new flood coverage. Existing policyholders may still have coverage, but they should expect significant premium increases or stricter renewal terms. It is highly recommended to contact your insurance broker to understand the specific conditions of your renewal in light of the new mapping data.

3. What is the 2026 high-risk zone mapping?

This is a comprehensive initiative by government and financial sectors to accurately identify and categorise geographic areas in Canada that face an unmanageable risk of climate-related disasters, specifically flooding. Properties falling within these high-risk red zones will face severe restrictions in obtaining private insurance coverage.

4. Can I still get a mortgage for a home in the Sumas Prairie?

Obtaining a mortgage for a new purchase in the Sumas Prairie will become exceedingly difficult. Major banks require comprehensive home insurance, including coverage against primary local risks like flooding, to approve a loan. Without access to new flood insurance policies, traditional financing avenues will likely be blocked for prospective buyers.

5. Is the government doing anything to help homeowners in these uninsurable zones?

Discussions are underway regarding the implementation of a national, state-backed flood insurance programme aimed at providing a safety net for those in high-risk zones. However, the framework is still in the developmental phase, and it remains unclear if it will be operational in time to offset the immediate impacts of the 2026 mapping rollout.